NWP Monthly Digest | May 2024

Saying goodbye to April shouldn't be difficult this year after yesterday's downbeat session in the stock market. This was the first month of negative returns for the stock market since October of last year. The stock market slump may come as a surprise as markets digested stronger-than-expected corporate earnings from the first quarter. Let’s not forget the stock market is up over 20% in the past year amid a thriving economy, a robust labor market, falling inflation, and an AI boom benefiting many companies outside of just semiconductors and software. Jamie Dimon, the CEO of J.P. Morgan, just referred to the U.S. economy as "unbelievable and booming." Yes, times are good!

What’s brewing under the surface?

Is the stock market taking a healthy pause to digest all of the data before ripping higher into the election season, or is something brewing under the surface? Outside of the financial world, a rare phenomenon is brewing under the surface. Over the next few weeks, two broods of periodical cicadas will emerge at the same time after spending about a year underground. If you’re like me, and had little knowledge on the subject. Cicadas resemble locusts, and although nearly all of the periodical cicadas in a given region emerge in the same year, the cicadas in different regions are not synchronized and may emerge in different years. All periodical cicadas of the same life cycle type that emerge in a given year are known collectively as a single “brood” (or “year-class”). In fact, the two broods (XIX and XIII) will emerge in 17 states, mostly in the Midwest and Southeast, for the first time in 221 years, and are not expected to do so again until 2245!

Lately, the economy continues to chirp like the male cicada while inflation has fallen within reach of the Fed’s 2% target after peaking in the fall of 2022. This may not seem unusual; a booming economy and falling inflation are like broods, and though each may occur in any given year, rarely do they emerge together. Rising inflation tends to coincide with a booming economy. Conversely, falling inflation tends to occur when demand and economic growth are waning. When times are good, consumers are healthy, and when consumers are healthy, they spend, pushing prices upward. The concept of a disinflationary boom is a rare spectacle due to its paradoxical nature. A strategist at J.P. Morgan noted this has only occurred in 1982 and 1991, and almost never before then.

What’s Really Going On Here?

As inflation dropped precipitously and approached the targeted levels set by the Federal Reserve, only a few components of the inflation data, like used car prices and homeowner's equivalent rent, were preventing inflation from falling further. In fact, after removing these components, the inflation rate was south of the Fed's 2% target. Meanwhile, the aggressive tightening by the Federal Reserve usually precedes a recession, and given those prospects, at the end of last year, investors were pricing in expectations that the Fed would cut rates six times in 2024, with the first cut coming in March. And who could blame them?

However, these were very optimistic expectations, and we've since learned they were unrealistic as the pace of the inflation descent has stalled considerably. Given widespread economic growth, it was only a matter of time before the data started to reflect what many Americans experienced during this prosperous time. Naturally, the Fed pushed back prospects of a rate cut into the summer, and now, after some hotter-than-expected data, there may not be any cut until the middle of 2024. Last month, Core PCE, which is the Personal Consumption Expenditures Index that strips out noisy components of inflation and is the Fed's preferred gauge, came in at 2.8% last week, above expectations and unchanged from the prior month. We also received economic data that provided a mixed outlook on the health of the economy. Prospects of a cooling economy and runaway inflation are reminiscent of the stagflation years that many baby boomers remember from the '80s.

And How Is the Stock Market Reacting?

The good news for the stock market is that it tended to react positively to the news about negative growth, as it implied the Fed could not remain unnecessarily restrictive for the foreseeable future. The reality is that the stock market can handle sticky inflation and delayed cuts from the Federal Reserve as long as those cuts are a matter of "when" and not "if." But if those discussions shift to whether or not the Fed will cut rates, prepare yourself for a sharp and knee-jerk reaction from the stock market.

We may have witnessed the market reaction to an “if” scenario as the stock market digested the inflationary data released yesterday morning. The S&P 500, the Nasdaq Composite, and the Dow Jones Industrial Average all lost more than 1.5%. In fact, all eleven sectors finished in the red. The latest piece of data suggesting inflation is running hotter than the central bank would prefer stemmed from housing prices rising 7% and more than expected, but the key report was the Employment Cost Index, which was at 1.2 percent quarter over quarter, compared to the 0.9 percent expected, insinuating further upward wage pressures. Not only does this measure allude to the fact that the Fed may not be able to cut in the near term, but it also insinuates longer-term inflationary pressures and a significant risk to the stock market if companies are unable to grow their bottom line while navigating increased costs of labor. That may warrant a reduction in price multiples for the stock market but also presents risks of a recession; as we all know, if wages are growing more than corporate profits, it would only be a matter of time before we witness widespread layoffs. While aggressive interest rate hikes have seemingly been effective, inflation is clearly stickier than previously thought. The prospect is that the Fed may not have the ammo to combat a resilient labor market, economic productivity, and healthy household balance sheets, which are all driving strong consumption. If the Fed finds itself fighting an uphill battle against inflation, using all the tools at its disposal to win the battle may be perilous and cost them the war, and now we have come full circle to the hard landing scenarios many priced in early last year.

When, and Not iF….

Given all the noise, we will hear from the Chairman of the Federal Reserve, Jerome Powell, to get some insight as to what the Fed is thinking. I'm optimistic Mr. Powell's comments will be pragmatic and along the lines of the progress made toward slowing inflation while recognizing their job is not done, but the Federal Reserve’s campaign to lower inflation still has a way to go to avoid the risk of cutting too early and repeating the mistakes from the 1980s. Investors will be reading between the lines for any developments hinting at prospects of the Fed shifting to "if," but we are confident Mr. Powell’s message should comfort investors that the cuts are still a matter of "when."

Is a Disinflationary Boom Still on the Table or Will This Aberration Self Correct?

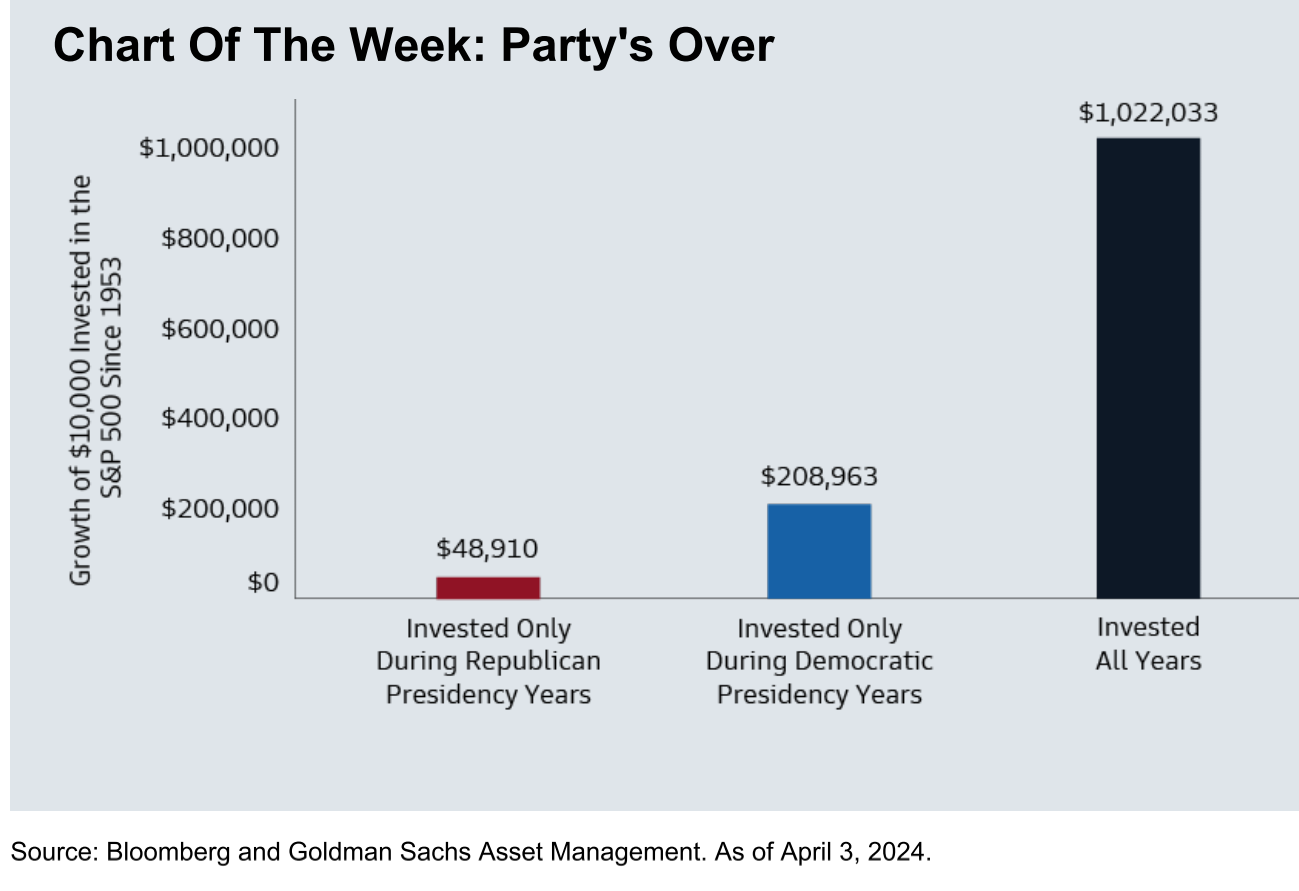

Perhaps both! We still believe a mild version of the disinflationary boom will play out, with inflation pressures rising, only to ultimately give way to long-term economic forces. Meanwhile, the resilient economy continues to demonstrate strength while ultimately falling to a natural and more sustainable rate of growth. In this environment, the stock and bond markets should do just fine. And “when” the Fed eventually cuts rates, it should come as welcomed news for investors. Perhaps, the strong economy and falling inflation decided to bury any bad brood between them, and they can go to this election party together. When the party is over, these economic relationships may go back into the dirt like the cicadas and return to normality the next time they emerge.

Noble Wealth Pro Tip of the Month

Party All the Time

Don’t worry about what type of party this November will bring. Just let loose and enjoy the ride. 😎

Regarding that topic, it might be wise to disregard the old saying, "sell in May and go away" this year. I'm generally skeptical about making investment decisions based on these so-called calendar year anomalies within the efficient market hypothesis. However, it's particularly crucial to avoid this strategy during election years.

Fun Facts of the Month

Tax Exam Shifts Gear Towards Financial Planning: This year, for the first time ever, between 30% and 40% of the questions on the “tax compliance and planning” discipline of the CPA exam will cover financial planning and cover topics like qualified retirement plans, investing, education funding and risk mitigation through insurance (Financial Planning).

An American Dream: Americans place a higher value on homeownership (78%) than any other metric in attaining financial stability. Of aspiring homeowners, 78% say that homeownership is unaffordable due to issues like insufficient income, high prices and lack of funds for a down payment (Bankrate).

Meta Woes: Meta Platforms (META) shed more than $100 billion in market cap on 4/25 in reaction to its earnings report on 4/24. It was the third time in META’s history that its market cap declined at least $100 billion in a single day. The only company to have reached that milestone more is Apple (AAPL), which has done it five times (Investopedia).

Postal Price Hike: On April 9, the US Postal Service filed a notice to increase the price of a first-class stamp from 68 cents to 73 cents. This would be the second increase this year and the fourth since the start of 2023. If approved, the price of a first-class stamp will have increased by 33% over the last four years (US Postal Service).

S&P 500 ETF Trading Tactics: Since 1993, when the S&P 500 ETF (SPY) began trading, a strategy of only owning the exchange-traded fund (ETF) on the day after more than 1% up days would have resulted in a cumulative price decline of 49%. The opposite strategy of only owning SPY on the day after more than 1% down days would have resulted in a cumulative price gain of 350% (Bespoke).

Costco’s Golden Opportunity: Costco began selling 1-ounce gold bars online in 2023, and Wells Fargo analysts now estimate that the retailer is already selling between $100 to $200 million worth of the yellow metal each month. On April 10, Costco reported March net sales of $23.5 billion, up 9.4% year over year (CNBC).

Tech Titan: The technology sector’s weighting in the S&P 500 is currently above 29%, which is four percentage points larger than the weighting of the smallest six sectors (out of 11) combined. Technology has now been the biggest sector in the S&P 500 for 17 consecutive years (S&P).

S&P 500 Triumphs: In the 12 months ended 3/31, the S&P 500 outperformed long-term (over 10 years) US Treasuries on a total return basis by 32.9 percentage points in what was the widest performance gap since December 2021 (Bespoke).

Manufacturing Mojo Returns: The ISM Manufacturing report rose more than expected in March, rising from 47.8 to 50.3. That ended a streak of 16 months of contractionary readings (sub-50), which was the third longest in the index’s history (since 1948).

Housing Heat Cools: After rallying 60% from April 2020 through October 2022, the median sale price of a new home in the US has now fallen 19.4% from $497k down to $400.5k as of February 2024 (US Census Bureau).

Automation Alters Work Landscape: In a quarterly CFO survey of businesses large and small, 51.1% said their firms have recently implemented automated tasks previously performed by employees. 37% of those firms have either laid off employees or slowed hiring as a result (Duke University, Richmond Fed).

Rent vs. Buy Battle: According to Realtor.com’s monthly Rental Report, in the 50 largest US metro areas, the monthly cost of buying a starter home was 60.1% ($1,027) more than the cost of renting. Across all 50 regions, renting is a cheaper option than buying. Metros where rent has the biggest advantage over buying include Austin, Seattle and Phoenix (Realtor.com).

What We’re Reading

Master of Change | Brad Stulberg

How do you respond to change? It’s not uncommon for people to react instinctively, as they yearn for the status quo, but the world is constantly changing and demands that we all develop a “rugged flexibility.” More importantly, the average person goes through 36 disorder events during their lives, which take the shape of the birth of a child, a promotion or layoff, marriage, death, and so on. People tend to respond to change in one of four ways: refusing to admit change is occurring; choosing to resist change; renouncing their agency; or trying to return to the pre-change status quo. These four responses stem from a misguided sense that life follows a pattern and reverting to the status quo mitigates discomfort. Instead of homeostasis, strive for allostasis, and achieve new stability by successfully adapting to change.

Resisting change releases cortisol, which increases the likelihood of inflammation, insomnia, metabolic issues, and other physical and psychological ailments. On a social level, resistance to change may give rise to demagogues and authoritarian figures as people gravitate toward figures claiming to bring back the old status quo—sound familiar?

Lessons of the book:

Develop a fluid sense of self

Be open to the flow of life

Alter your expectations to better align with reality

Practice your core values

Respond thoughtfully instead of reacting instinctively (Use the four Ps: Pause, process, plan, proceed)

Don't attempt to derive immediate meaning from every painful experience